A review of key brand visibility metrics across 10 holiday gift categories during the critical holiday sales window.

To download the report, fill out the form below:

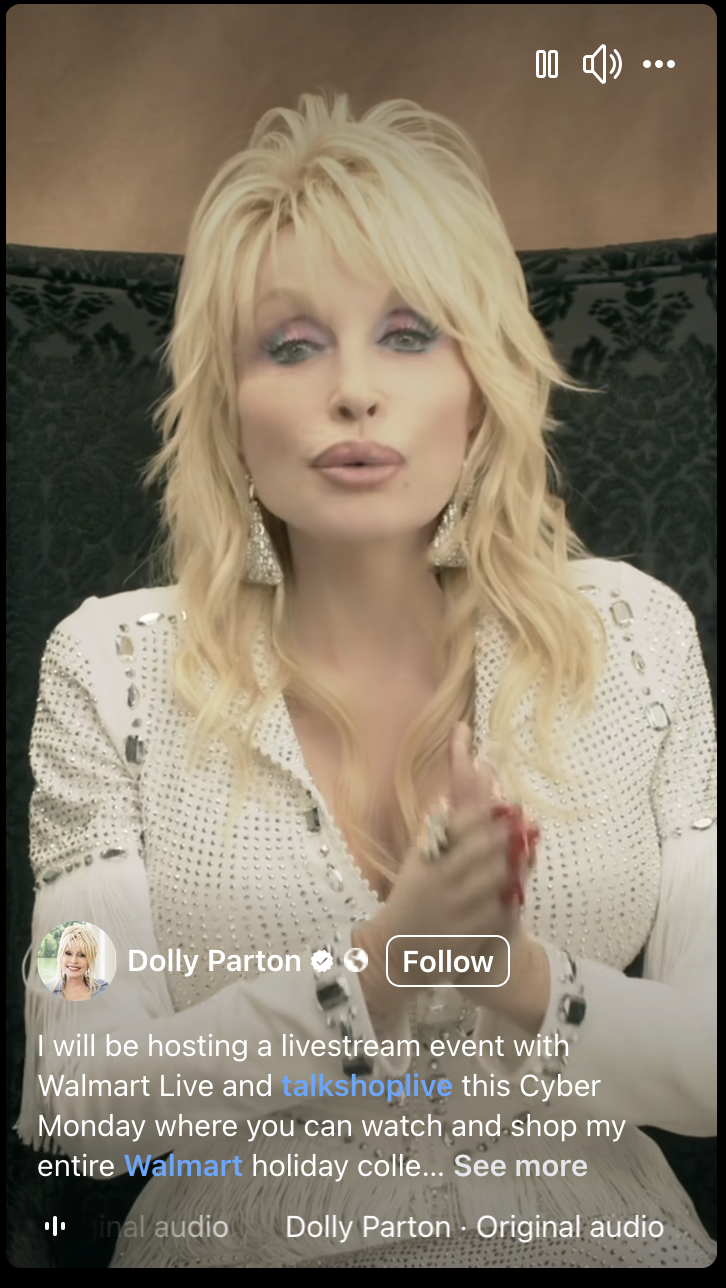

All that shopping — and Dolly Parton, too.

Online spending over the critical Cyber 5 sales window reached new heights this year, with U.S. consumers setting records every day from Thanksgiving to Cyber Monday.

By the time the dust had settled and the sales were (mostly) over on Monday night, consumers had racked up an estimated $41.1 billion in receipts over the five-day period, an 8.2% increase compared with 2023, according to Adobe Analytics. That total included daily tallies of:

- $13.3 billion on Cyber Monday, an increase of 7.3%. Consumers charged (or maybe Paypalled?) $15.8 million every minute between 8 p.m. and 10 p.m., Adobe estimates.

- $6.1 billion on Thanksgiving, a rise of 8.8%.

- $10.8 billion on Black Friday, up 10.2%.

- $10.9 billion on the as-yet-unnicknamed holiday weekend, an increase of 5.8%. year-over-year).

The activities even turned star-studded on Monday night, when Walmart Live hosted a special-edition shoppable livestream with country music legend Dolly Parton (who has an exclusive product line at the retailer).

The most popular product categories during the sales window included toys, electronics, apparel, personal care items and jewelry. On the list of top-selling items were computers and laptops, digital cameras, TVs, Bluetooth headphones and speakers, skin care and makeup, and electric scooters and bikes.

Discounts across most of these categories rose well above 20%. And the average discount overall was 28% — down 3% from 2023, according to Adobe. Also noteworthy is that more than 50% of online sales during the period came through mobile devices.

TRACKING BRAND PERFORMANCE

Using data generated by our Marilyn Ecommerce Insights Suite, Mars United has compiled an exclusive special report examining visibility trends in 10 of the most popular gifting categories during the Cyber 5 sales event at the nation’s two leading online retailers, Amazon.com and Walmart.com.

The report presents a clear picture of the brands that earned — or paid for, as the case may be — the greatest visibility at Amazon and Walmart during this critical holiday sales window.

But it also illustrates how much shopping behavior and brand activity differ across these two leading retailers. In fact, only six of the 100 most successful brands (based on estimated share of sales) across the 10 categories were the same at Amazon and Walmart:

- Apple in Electronics,

- Energizer in Household Essentials,

- Lego and Mattel’s Barbie in Toys, and

- Nintendo and PlayStation in Video Games.

Even the brands involved in paid sponsorships and promotional executions varied widely at each retailer, as both national brands and smaller, niche players seemed to focus their investments on one retailer more than the other. (This isn’t always the case, of course. In Electronics, for example, Apple, Samsung, and Sony were heavy promoters and sponsors on both websites.)

While that trend obviously reflects a substantial difference in brand availability on each website (especially given Amazon’s larger inventory), it also suggests that many brands take different approaches to advertising at each retailer based on their marketplace position and business objectives.

GENERAL TRENDS

Apple was a clear (if unsurprising) winner, as it claimed the top spot in terms of share of sales growth at both Amazon and Walmart in the Electronics category and, thanks to its line of watches, also placed first in the Clothing, Shoes & Jewelry Category at Amazon. The Electronics category leader was extremely visible in paid activity at both retailers as well.

Only two other national brands figured prominently in more than one of the 10 categories covered in this report: audio brand Tikland, which, like Apple, ranked in both Clothing, Shoes & Jewelry and Electronics — although at Walmart; and battery maker LiCB, which ranked fourth for share of sales growth in Home Improvement and first in Household Essentials at Walmart. Private label Amazon Basics, meanwhile, turned up in three categories.

Sales Growth vs. Paid Activity

Aside from a handful of cases, there isn’t much discernible direct correlation between sponsorship/promotional activity and share of sales growth in the report. For example, although LiCB gained heavy exposure through paid efforts in Household Essentials (top five for both promoted items and sponsorship activity) at Walmart, it was significantly less prominent for those areas in Home Improvement.

One clear exception came in the Pet Supplies category at Amazon, where four of the five top brands for share of sales growth were also among the five most-sponsored brands: Blue Buffalo, Greenies, Amazon Basics, and Purina Pro Plan. And in Toys, Lego gained strong exposure through paid search results at both retailers and ranked first in sales growth at Amazon and second at Walmart.

Less Room for Small Brands

Well-known national brands were far more prominent at both Amazon and Walmart during Cyber 5 than they usually are during tentpole sales events at Amazon, especially in the Pet Supplies, Toys, and Video games categories. While established brands typically rise to the top visibility-wise at Walmart, lesser-known brands with Amazon-focused distribution strategies often steal the show there.

One case in point: In Home Improvement, China-based home goods brand Bedsure ranked highly for share of sales growth as well as promotion and sponsorship activity.

Black Friday vs. Cyber Monday

“Cyber Monday” promotions were far more common across these 10 categories over the course of the weekend than “Black Friday” offers, which were more popular in only two cases at Walmart: Clothing, Shoes & Jewelry and Sports & Outdoors.

Despite shopper expectations for massive discounts during Cyber 5, the average discounts on best-selling items were notable lower than the national averages cited by Ado in many cases. For instance: 7.7% at Amazon and 11.7% at Walmart for Clothing, Shoes & Accessories; 12.5% for Electronics at Walmart and 11.5% for Video Games at Amazon.

Category-Specific Trends

In Toys, along with Lego’s dominant performance, Barbie finished in the top 5 for sales growth at both retailers without corresponding levels of paid placement. And Disney scored a top-five slot in sales growth and did the same in sponsorship activity.

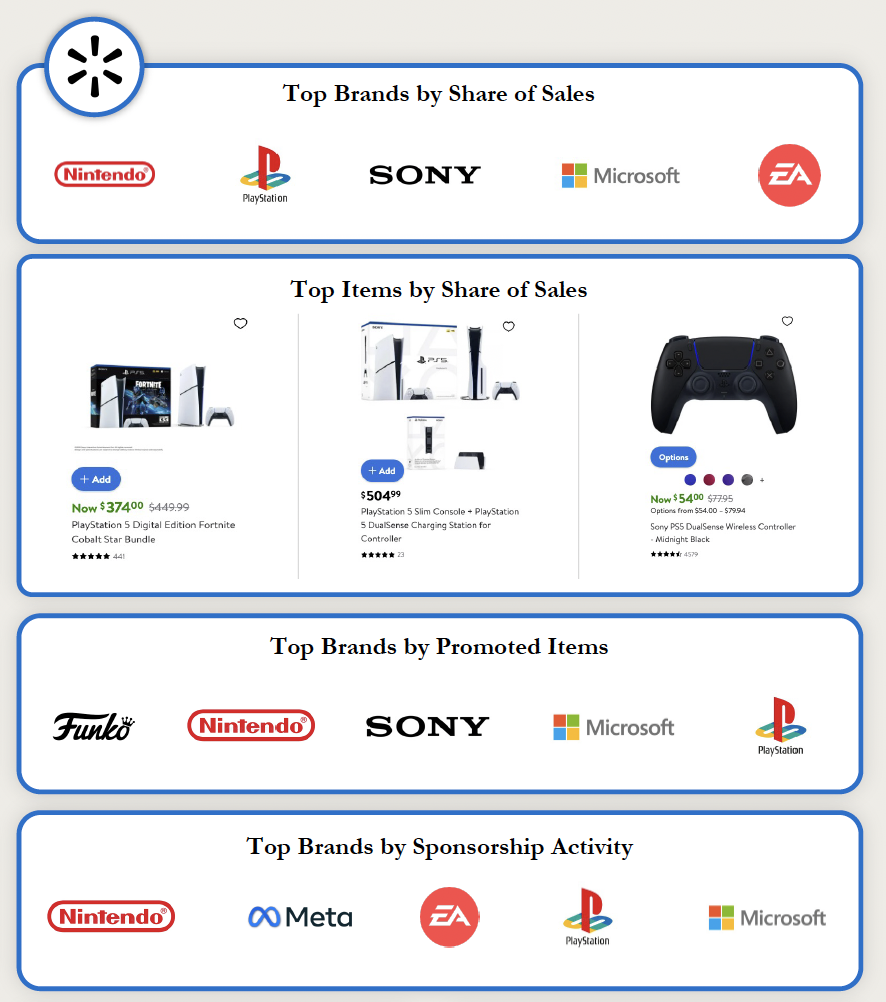

In Video Games, Nintendo, PlayStation, and Microsoft were among the five most active brands for both promotions and sponsorships at Walmart, where they proved to be another exception to the trend mentioned earlier by also landing in the top five for share growth. EA, too, hit the top five for both sponsorship and share growth.

Meanwhile, PlayStation and Nintendo placed in the top five for sales growth at Amazon without ranking among the top five in either of the paid lists.

To download the report, fill out the form below:

Eligible marketers can learn how their own brands performed during Cyber 5 by using a new, first-of-its-kind free performance recap tool from the Marilyn Ecommerce Insights Suite. Qualified brands can also receive a more complete audit of their performance conducted by a member of the Mars United Ecommerce team.